How Divorce Housing Strategy Works

Divorce Housing Strategy introduces a structured approach to evaluating housing decisions before settlement agreements are finalized.

Housing decisions made during divorce often involve legal, financial, and lending considerations that do not naturally align.

This framework brings structure to that process.

A Structured Approach to Housing Decisions in Divorce

Divorce Housing Strategy organizes housing decisions during divorce into a structured process that aligns financial feasibility, settlement terms, and long-term housing sustainability.

Divorce Housing Strategy integrates legal settlement structures, financial feasibility, and mortgage capacity considerations into a coordinated housing evaluation framework.

Why Housing Decisions Often Break Down During Divorce

Divorce settlements frequently determine who receives the home.

Mortgage qualification, however, is determined separately.

Courts allocate property.

Attorneys negotiate settlement terms.

Lenders evaluate financial feasibility.

When these systems operate independently, expectations and financial reality can diverge.

Divorce Housing Strategy introduces a framework designed to evaluate housing feasibility before decisions become permanent.

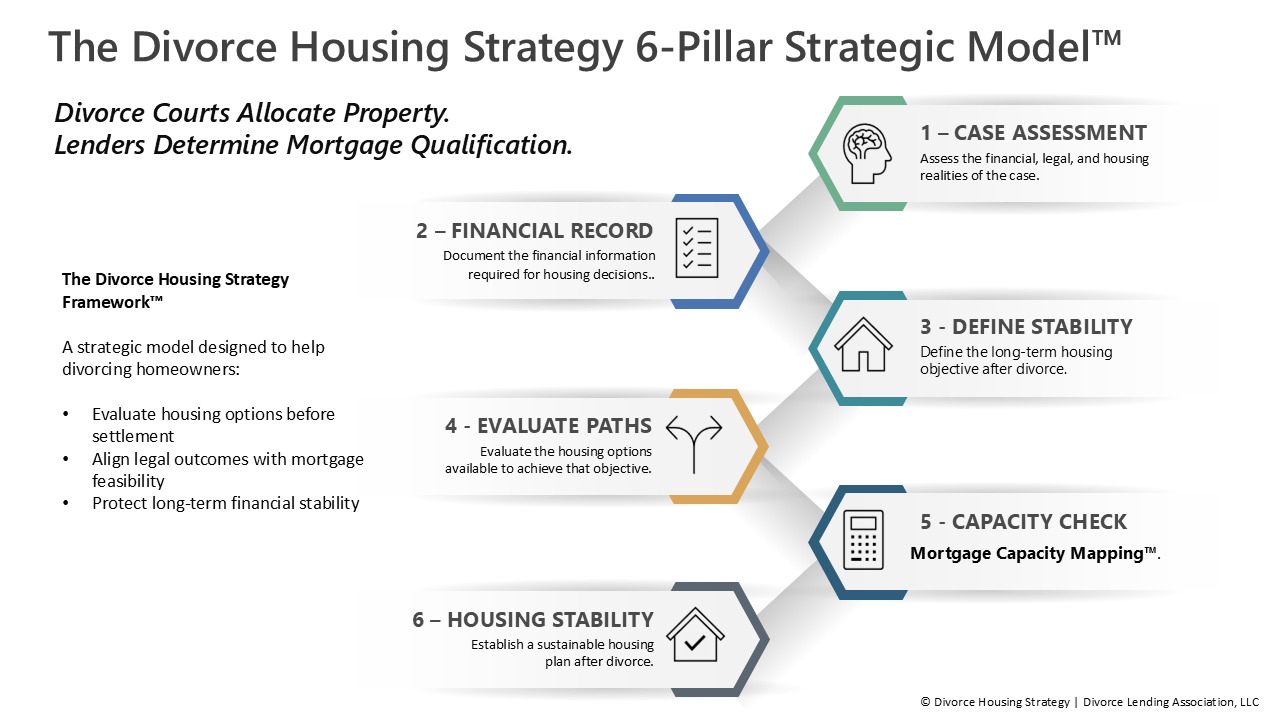

A Structured Three-Stage Process

Divorce Housing Strategy organizes housing decisions into a structured evaluation process.

This framework allows individuals and professionals to move from uncertainty toward informed decision-making.

The process unfolds across three stages.

.

Stage 1 — Clarity Before Commitment

Before housing decisions are embedded into settlement agreements, the financial variables influencing feasibility should be organized.

The Divorce Housing Strategy Clarity Session™ introduces a structured evaluation process that helps individuals:

- document income and debt

- evaluate refinance feasibility

- assess housing sustainability

- identify structural questions

- prepare for professional

- conversations

This stage helps individuals think clearly before commitments are finalized.

Begin with the Clarity SessionStage 2 — Mortgage Capacity Strategy Review™

When housing decisions are incorporated into settlement agreements, expectations must be tested against financial feasibility.

The Mortgage Capacity Strategy Review™ applies the Mortgage Capacity Mapping™ methodology to evaluate whether a proposed housing outcome aligns with lending feasibility and long-term financial sustainability.

This evaluation is conducted by a Certified Divorce Lending Professional (CDLP®) and results in a Divorce Mortgage Planning Report™ outlining the structural housing considerations influencing settlement planning.

Begin the Mortgage Capacity Strategy ReviewStage 3 — Professional Implementation

Once a housing path is determined, implementation requires coordination between legal, financial, and lending professionals.

Certified Divorce Lending Professionals (CDLP®) specialize in the intersection of:

- divorce settlement structures

- mortgage qualification realities

- real property considerations

These professionals work alongside attorneys and financial professionals to help ensure housing decisions remain aligned through execution.

Why Structure Matters

Housing decisions made during divorce can influence financial stability for years.

When decisions are made without evaluating qualification capacity, debt allocation, and timing considerations, unexpected complications can emerge.

Divorce Housing Strategy introduces structure into this process so housing decisions are evaluated with clarity rather than assumption.

Structure First. Commitment Second.

Housing decisions made under pressure often unravel.

Housing decisions made under structure hold.

Begin the Clarity Session