Why Housing Decisions Fail in Divorce

Divorce settlements often determine who receives the home, but financial feasibility determines whether that decision holds.

Housing decisions during divorce involve more than property division.

They must align legal settlement terms, financial restructuring, and mortgage capacity.

When these elements are evaluated separately, housing outcomes that appear workable during negotiations can later prove financially unsustainable.

Understanding why these decisions fail is the first step toward evaluating housing feasibility more effectively.

The Structural Gap in Divorce Housing Decisions

Divorce proceedings frequently address the allocation of real property.

However, the legal settlement process does not determine mortgage qualification or long-term housing sustainability.

Housing outcomes must ultimately align with financial realities such as:

• income documentation

• debt obligations

• credit exposure

• refinance eligibility

• payment sustainability

When these factors are not evaluated alongside settlement planning, housing decisions may fail after agreements are finalized.

This gap between legal allocation and financial feasibility is where many housing challenges during divorce originate.

The Three Structural Failures

Failure 1 — Settlement Terms That Cannot Be Financed

Divorce agreements may assume a refinance will occur within a specific timeframe.

However, mortgage feasibility depends on financial qualification standards that are independent of settlement language.

Without evaluating those standards in advance, refinancing expectations may not align with financial reality.

Failure 2 — Income That Cannot Be Treated as Expected

Income used in settlement negotiations may not always meet the documentation or stability requirements used to evaluate mortgage capacity.

Support income, variable earnings, or self-employment income can all influence how housing feasibility is assessed.

Understanding how income structure affects housing capacity is essential before commitments are finalized.

Failure 3 — Debt That Was Never Structurally Reallocated

Divorce settlements frequently reassign responsibility for debt.

However, reassignment does not always remove financial liability from credit reports or lending evaluations.

Joint obligations or unresolved liabilities can affect borrowing capacity even when settlement agreements assign payment responsibility elsewhere.

Why Housing Decisions Require Structural Evaluation

Housing feasibility during divorce exists at the intersection of three systems:

• legal settlement planning

• financial restructuring

• mortgage capacity

These systems are often managed by different professionals, each focusing on their area of expertise.

When housing decisions are evaluated within only one of these systems, critical structural factors can be overlooked.

A coordinated evaluation helps ensure that housing expectations align with financial feasibility before settlement commitments are finalized.

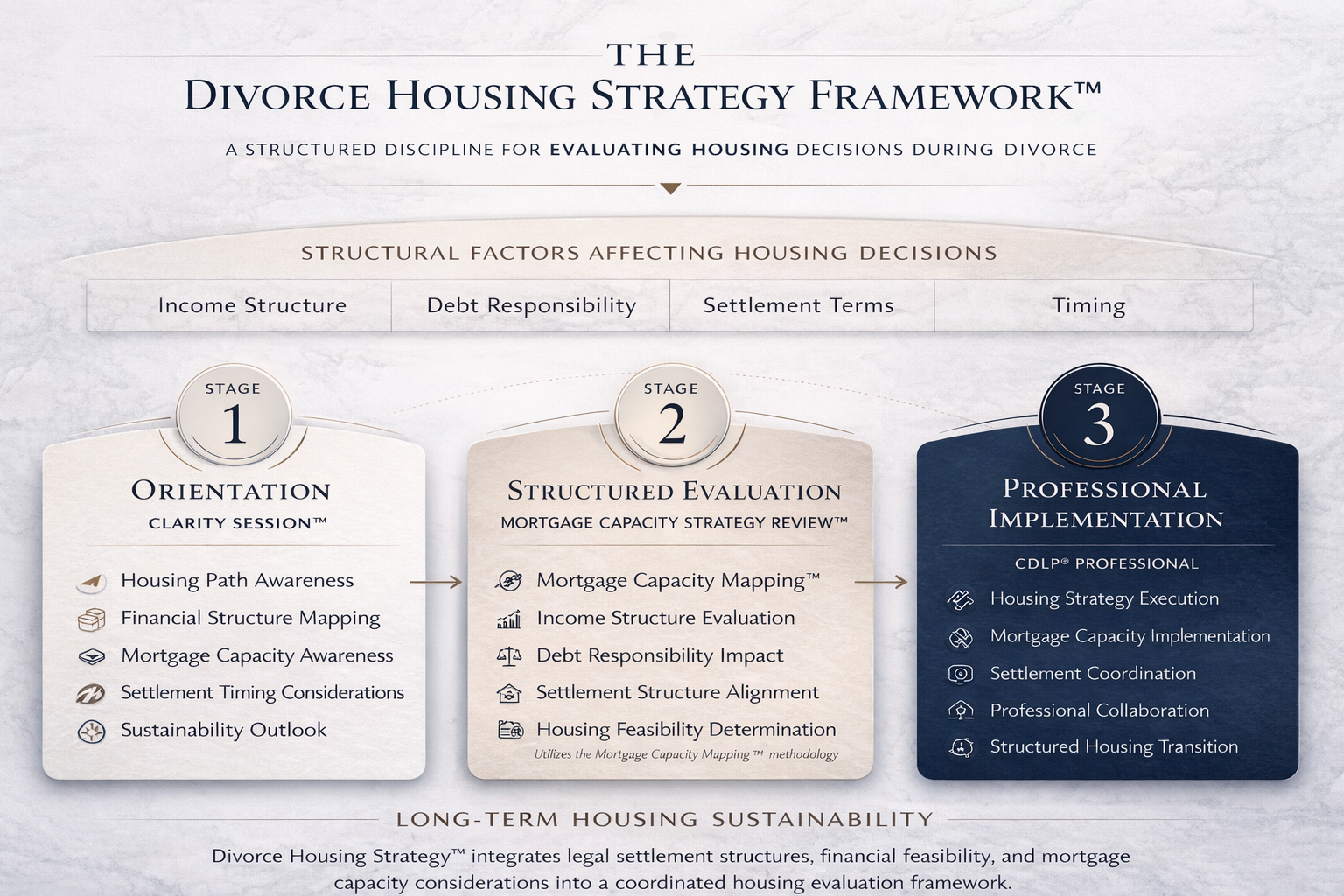

This structured approach is explained through the Divorce Housing Strategy Framework™.

Structural Evaluation in Divorce Housing Planning

Housing feasibility during divorce is influenced by several structural variables that must align before housing decisions can be sustained long-term.

These variables often include:

• income structure and documentation

• debt responsibility and credit exposure

• settlement structure and timing

• refinance feasibility

• payment sustainability

Evaluating these factors together helps determine whether a housing outcome remains financially viable once the divorce process is complete.

This type of coordinated evaluation is commonly referred to as Divorce Mortgage Planning.

The Divorce Housing Strategy Framework™

Divorce Housing Strategy organizes housing decisions into a structured process designed to evaluate financial feasibility before commitments are finalized.

Divorce Housing Strategy™ integrates settlement structure, financial feasibility, and housing capacity considerations into a coordinated evaluation framework.

Where Most People Begin

For individuals navigating divorce, the first step is often gaining clarity around how housing decisions interact with financial realities.

Divorce settlements may determine who receives the home, but housing sustainability ultimately depends on financial structure — including income, debt responsibility, settlement timing, and mortgage capacity.

Before commitments are finalized, many individuals begin by evaluating these structural factors to understand whether a proposed housing outcome is financially feasible.

This orientation helps individuals approach housing decisions with greater awareness and prepares them for more informed conversations with legal and financial professionals.

Begin With Structured Orientation

The Divorce Housing Strategy Clarity Session™ provides a structured 60-minute orientation designed to help individuals evaluate the key financial factors that influence housing decisions during divorce.

This guided session introduces the structural considerations that determine whether a housing path is financially sustainable before settlement commitments are finalized.

The session includes:

• housing path awareness

• financial structure mapping

• mortgage capacity awareness

• settlement timing considerations

• sustainability outlook

This orientation helps individuals understand how housing decisions interact with financial structure so they can approach the divorce process with greater clarity and confidence.

Begin the Clarity SessionThe Clarity Session introduces the structural principles used within the Divorce Housing Strategy Framework™.

Housing evaluation during divorce often benefits from collaboration between legal, financial, and housing professionals.

Learn more about professional collaboration within Divorce Housing Strategy.

Structure First. Commitment Second.

Housing decisions made under pressure often unravel.

Housing decisions made under structure hold.

Start With the Clarity SessionWhen a Deeper Evaluation Is Needed

When housing decisions are embedded into settlement agreements, a more structured evaluation may be required.

Divorce Housing Strategy™ was developed within the Divorce Lending Association to address the structural gap between settlement planning and mortgage feasibility.